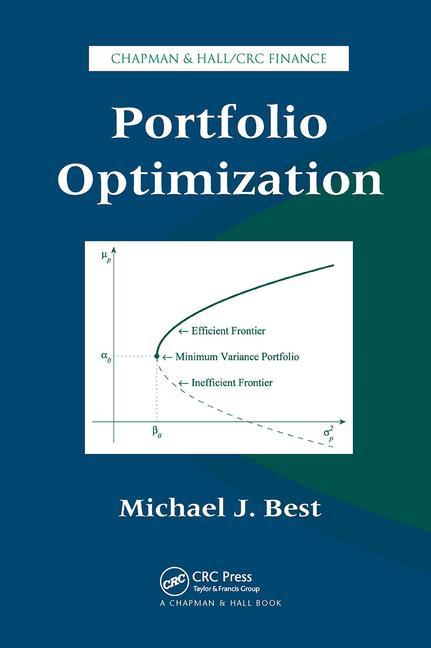

Portfolio Optimization

Autor:

Michael J. Best

Dostępność:

50 % szansa

Przeszukamy cały świat

339.57

zł

Eschewing a more theoretical approach, Portfolio Optimization shows how the mathematical tools of li...